-

Abstract:

Estimations and applications of factor models often rely on the crucial condition that the number of factors is consistently estimable, which in turn also requires that factors be relatively strong, data are stationary, and the sample size be fairly large, although in practical applications, one or several of these conditions may fail. In these cases it is difficult to analyze the eigenvectors of the original data matrix. To address this issue, we propose simple estimates of the factors using cross-sectional projections of the original datasets, by weighted averages with pre-determined weights. These weights are chosen to diversify away the idiosyncratic components, resulting in ``diversified factors". Because the projection is conducted cross-sectionally, it is also robust to serial dependence conditions. We formally prove that this procedure is robust to over-estimating the number of factors, and illustrate it in several applications. We also recommend several choices for the diversified weights. When they are randomly generated from a known distribution, we show that the estimated factor components are nearly optimal in terms of recovering the low-rank structure of the factor model.

- Paper:

pdf file

- Supplement:

pdf file

- Simulation: forecast:

Matlabcode1

Matlabcode2

- Simulation: treatment inference using diversified projection:

Matlabcode1

Matlabcode2

Scenario I: The high dimensional control variables X have a factor structure with r=2 factors. R is the used number of factors for Diversified Projection (DP). "double selection" uses double Lasso directly on X without estimating factors.

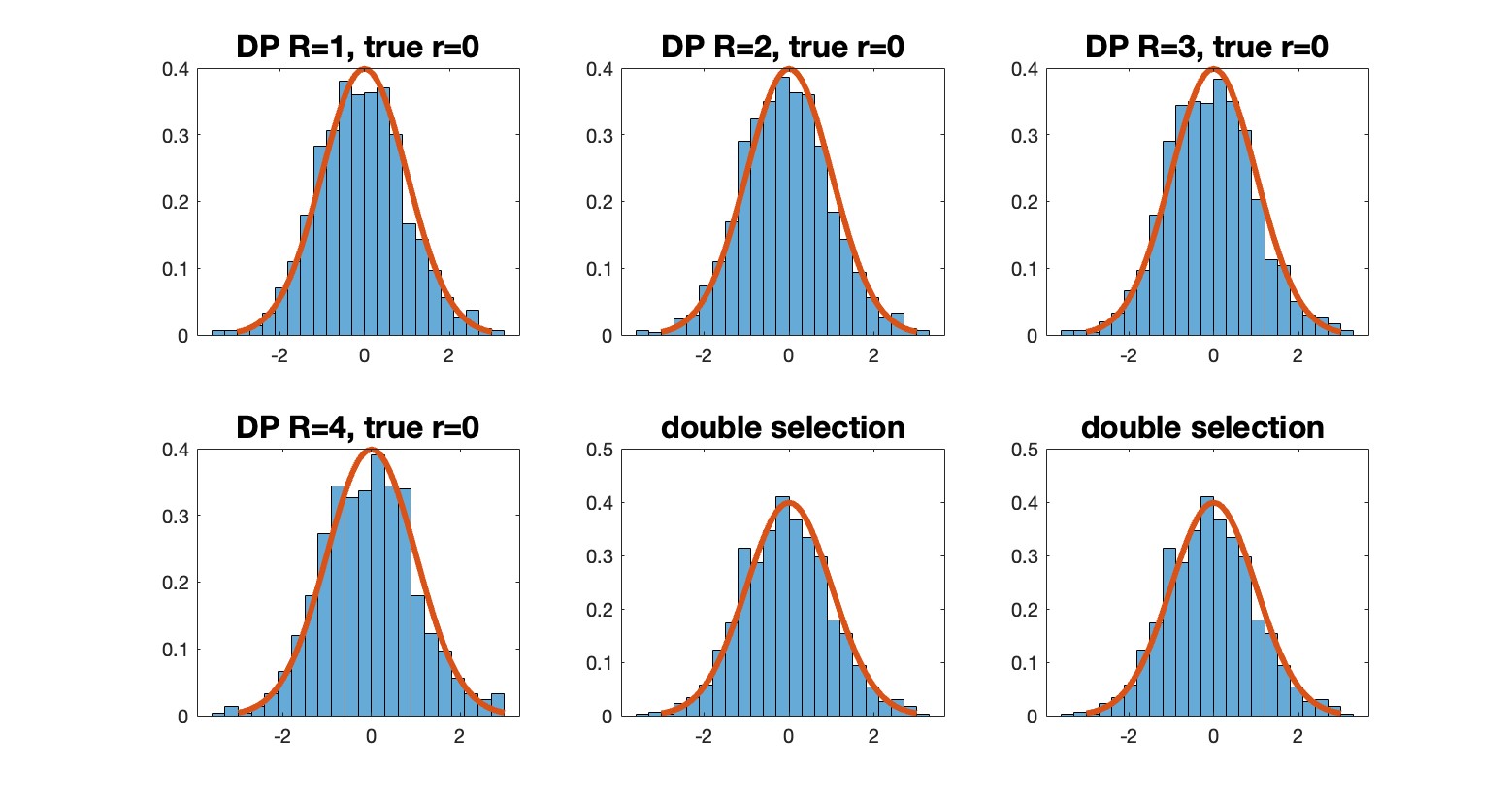

Scenario II: The high dimensional control variables X have no factor structure (r=0 ) . R is the used number of diversified projections. "double selection" uses double Lasso directly on X without estimating factors.