-

Abstract:

No, and often it helps !

- Paper:

The paper

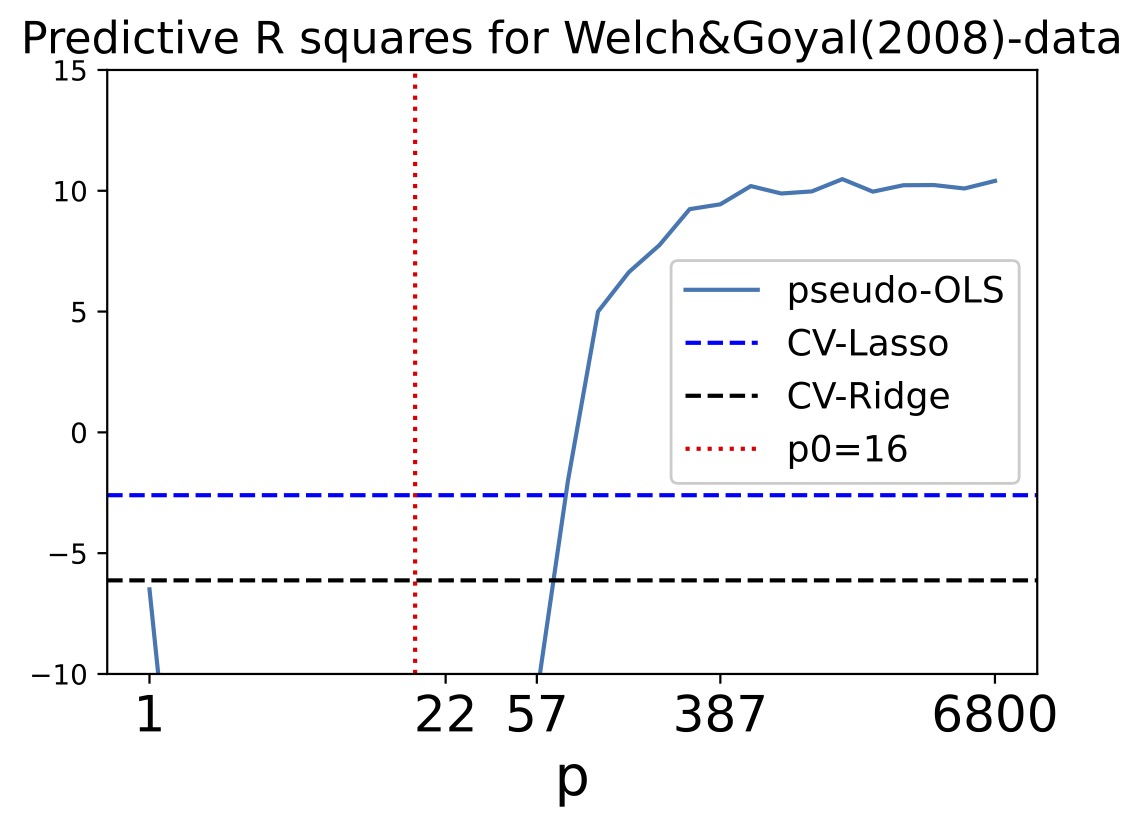

- Forecasting annual U.S. equity premium:

Sixteen predictors described by Welch and Goyal (2008).

The predictive R square as the number of predictors p increases. The original dataset contains p0=16 predictors. So all the remaining p-16 predictors are artificially added standard normal noises. The predictive R square stabilizes at around 10 percent after 300 ~ 6,800 noises have been artificially added. The predictor is simply pseudo-OLS:

x'new(X'X)+X'Y

where the pseudo inverse is used to replace the ordinary inverse in OLS.